The Algorithm Ate the Playlist (And Nobody Asked What Comes Next)

A Guide To... Why The Most Sophisticated Listener Intelligence System Ever Built Has Produced Zero Tools for Artists

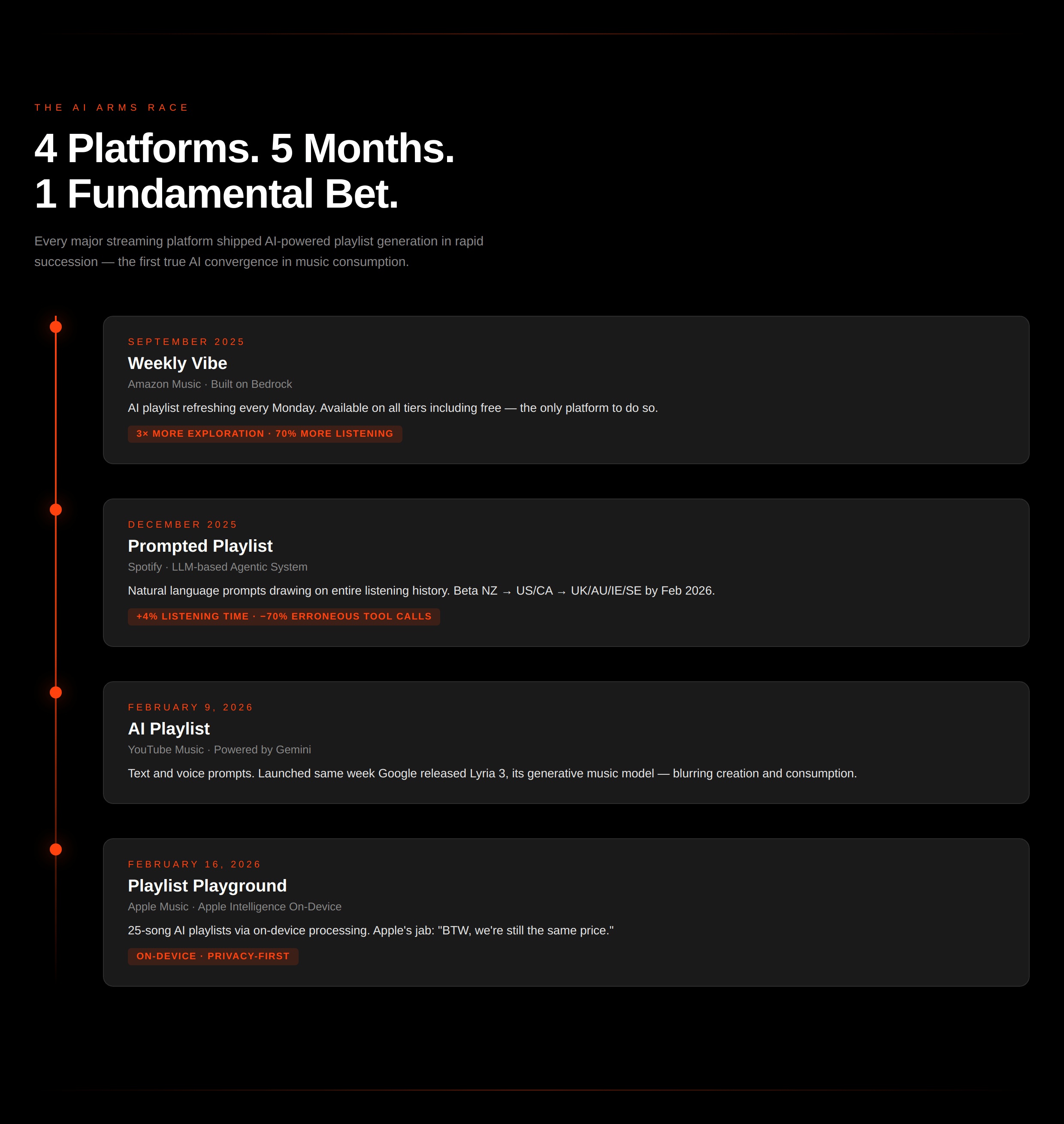

Four platforms. Five months. The same fundamental bet; that natural language will replace browse-and-search as the primary mode of music discovery, yet Spotify became the flashpoint for one of the most spectacular corporate-influencer misfires in recent memory.

Spotify paid several prominent Australian music industry figures to promote the feature. The community’s response was immediate, overwhelming, and brutal. Comment sections became communal exorcisms, with artists and fans competing to extend the mockery.

The frustration is real and it’s earned. But fixating on one company’s rollout obscures the far more significant reality; every major streaming platform converged on AI-driven discovery within the same five-month window, and that convergence tells you everything about where the industry is heading. The strategic question isn’t whether AI playlists are good or bad. It’s why the most sophisticated listener intelligence system ever built has produced zero native tools for artists to monetise the relationships that data reveals.

Every Major Platform Shipped AI Playlists Within Five Months But There’s Still No Data To Access…

The Australian backlash has been framed almost entirely as a Spotify story. But fixating on Spotify obscures that every major streaming platform has shipped AI features within a five-month window, and the convergence tells you far more about the industry’s trajectory than any single company’s ethics.

Amazon Music moved first with Weekly Vibe in September 2025. Spotify’s Prompted Playlist beta-launched in New Zealand in December, reaching Australia by late February. YouTube Music launched its AI Playlist (powered by Gemini) on 9 February 2026, the same week Google released Lyria 3, its latest generative music model, blurring creation and consumption in ways that should concern anyone paying attention. Apple Music arrived with Playlist Playground in the iOS 26.4 developer beta on 16 February.

Four platforms. Five months. The same fundamental bet: that natural language will replace browse-and-search as the primary mode of music discovery. Music Ally framed the shift as “Musical SEO”; the idea that an artist’s discoverability will increasingly depend on how well their metadata, descriptions, and catalogue are optimised for AI interpretation. I’ve also written extensively about how recommendation engines actually work and the depth of Spotify’s data intelligence operation. My pieces laid out the multi-layered systems underpinning music discovery within Spotify and comparable platforms. And understanding that infrastructure is the prerequisite for understanding what Prompted Playlist represents beyond its controversial rollout.

All in all the system generates diverse playlist candidates, scores them using a reward model calibrated against long-term listening satisfaction (not just click-through rates), and fine-tunes using “Direct Preference Optimisation.” Spotify explicitly notes they accept short-term engagement trade-offs to achieve better long-term retention, a fundamentally different optimisation target than most people assume. Their internal testing showed that optimising for discovery drops immediate satisfaction by 8.75% but increases discovery by 36.19%, with significantly boosted streams to emerging and catalogue artists.

Whether you think that’s exciting or dystopian, it’s happening regardless.

What’s missing from the conversations and discourse is how the system rewards depth of engagement over breadth. From Spotify’s developer notes, artists who generate deep listener responses, even to smaller audiences, receive algorithmic amplification that artists with shallow, high-volume play counts don’t. This is great on paper, but the issue comes down to access and ownership of data, which underpins creative strategies…

That’s a metadata problem, a catalogue optimisation problem, and a policy advocacy problem. It’s solvable. But it requires engagement with the technology, not rejection of it.

This is the argument the Australian music industry should be having about the use of AI within DSPs but why the most sophisticated listener intelligence system ever built has produced zero native tools for artists to monetise the relationships that data reveals. Joel Gouveia’s crystallisation of the structural critique is something I agree with deeply;

“Spotify does not want you to have a relationship with your fans. Spotify wants your fans to have a relationship with Spotify.”

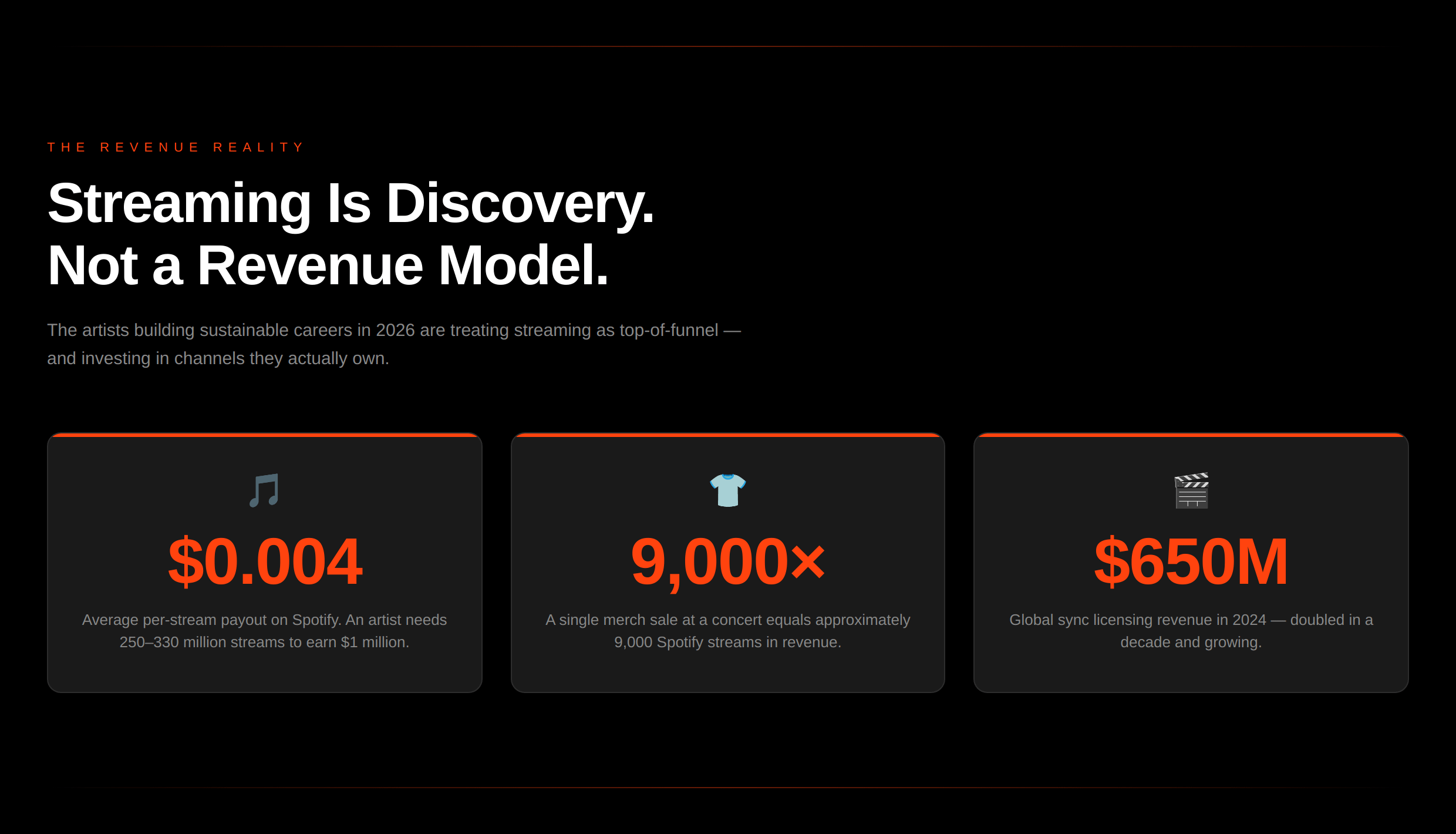

Let’s be precise about why this matters economically. The revenue breakdown for working artists in 2026 is stark. An artist needs roughly 200–330 million streams to generate $1 million from the platform alone. Meanwhile, a single merch sale at a concert equals approximately 9,000 Spotify streams. Sync licensing reached $650 million globally in 2024 (IFPI). The money in music is everywhere except streaming royalties; and yet streaming is where the deepest fan intelligence sits, locked behind a platform that has no commercial incentive to share it.

Is There An Alternative?

An ecosystem of direct-to-fan tools has matured in response to this structural absence, and the economics are compelling even at small scale.

Laylo (used by Fred again.., Calvin Harris, ODESZA) now facilitates over $1 billion in revenue from drops. James Blake’s Vault ($5/month for unreleased tracks) generates revenue equivalent to 600,000 Spotify streams from just 500 subscribers. Medallion FM launched a user-centric streaming service at $4.99/month where 85% goes to artists, with complete fan CRM data. Venice Music, founded by former Lady Gaga manager Troy Carter, offers AI-powered career management alongside distribution. Pomplamoose earns $15,000/month from 2,500 Patreon supporters, equivalent to royalties on 4 million monthly Spotify streams, with zero label recoupment.

But let’s be honest about the limitations. The structural problem is that the D2F ecosystem is building around the platforms rather than within them. Every tool in the space; Laylo, Patreon, Bandcamp, Discord, Vault requires the artist to get a listener off the streaming platform and onto a separate service. That’s a conversion funnel with enormous drop-off. Ben at STVDIO, (fellow Substack writer and one of the sharpest analytical voices in the space) has also documented that major labels are dominating direct-to-fan sales more than all others combined…

D2F isn’t a silver bullet. It’s not replacing streaming, but it is an additional connection point for fan connection and monetisation. The platform that closes this gap that connects discovery-level behavioural intelligence with native monetisation infrastructure doesn’t just capture the superfan market. It restructures the entire value chain… And we’ve seen it done.

It’s Not All Doom & Gloom…

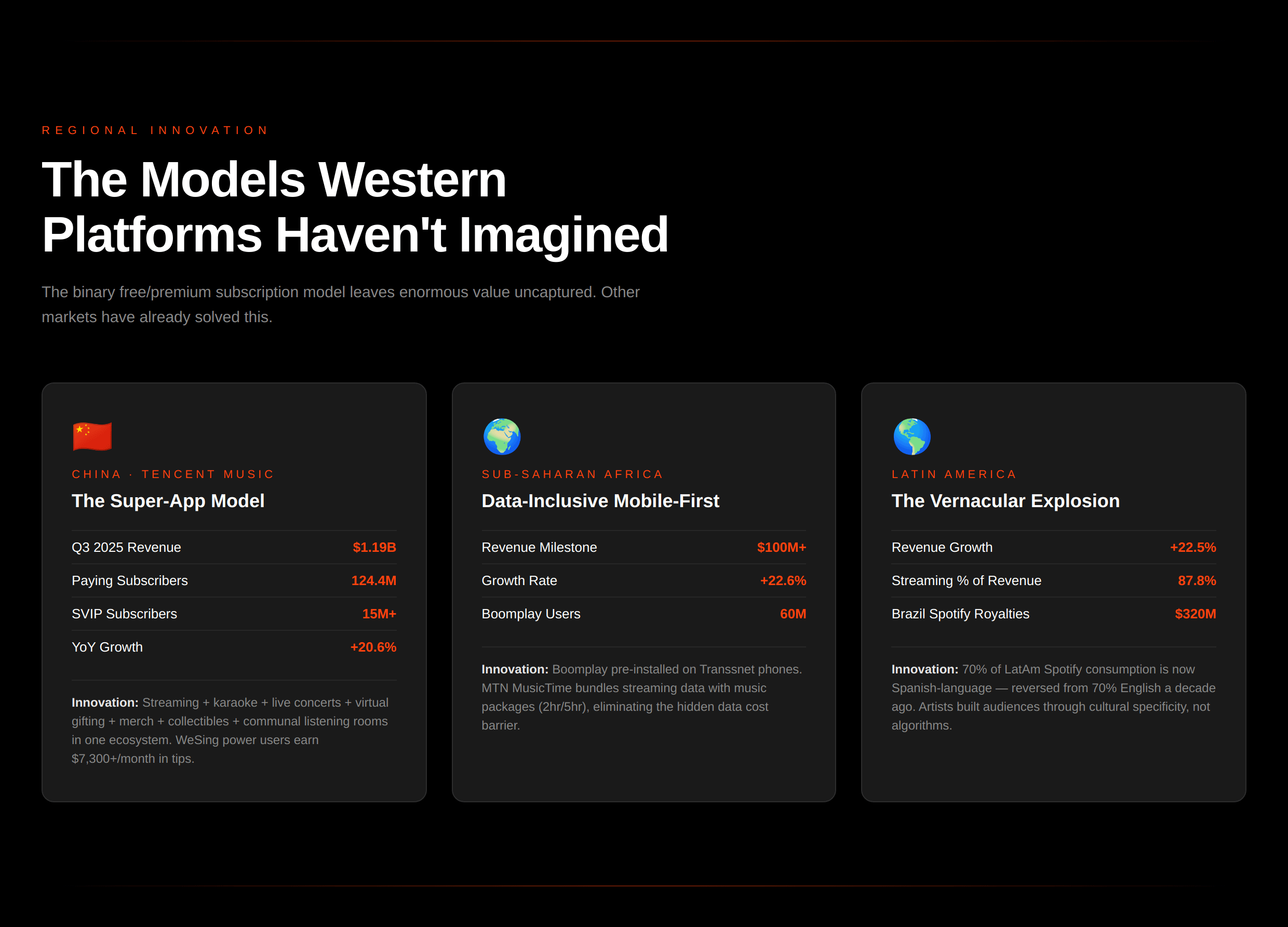

Whilst the anglosphere argues, other markets have already built the integrated models.

China’s Tencent Music Entertainment platforms (QQ Music, Kugou, Kuwo, and WeSing) integrate streaming, karaoke, live-streamed concerts, virtual gifting, digital album collectibles, artist merchandise, and real-time communal listening rooms into a single ecosystem. In Q3 2025, TME reported RMB 8.46 billion ($1.19 billion) in revenue, up 20.6% year-over-year, with 124.4 million paying subscribers. Its SVIP (”Super VIP”) tier surpassed 15 million subscribers, offering premium audio, early concert tickets, and exclusive collectible cards at roughly five times the standard subscription price. WeSing power users earn $7,300+ per month in virtual tips. Comments under tracks on NetEase Cloud Music (another Chinese streaming service) function as mini-forums where users share personal stories, creating emotional engagement that no Western platform replicates (besides SoundCloud).

I’m sorry to the optimists out there but Tencent, Netease and other platforms didn’t build this infrastructure as a philosophical statement about artist empowerment. It built it because integrated monetisation generates more revenue per user than subscriptions alone. They’re the primary revenue architecture.

Other regional models include Sub-Saharan Africa which crossed $100 million in recorded music revenue for the first time, growing 22.6%. Boomplay (60 million active users) solved distribution by coming pre-installed on Transsnet phones. MTN MusicTime pioneered data-inclusive bundles where users purchase 2-hour or 5-hour music packages with streaming data included, eliminating the hidden cost barrier that makes a $10.99/month subscription irrelevant in markets where mobile data costs more than the music itself.

Apple Music’s TikTok partnership (announced February 2026) represents one of the few genuinely forward-looking Western moves; full-song streaming without leaving TikTok, and real-time “Listening Parties” with artist-hosted chat. Beta tests with SZA, Bad Bunny, and Charli XCX reportedly drew tens of thousands of simultaneous participants. It’s the first serious attempt to close the discovery-to-listening gap. But it’s still a partnership between two separate platforms; a bridge, not an integrated experience.

Playing the Game…

The architecture I’ve laid out above has direct implications for how artists, labels, managers, and industry bodies should be positioning themselves right now. Not because of the Prompted Playlist or Spotify specifically; that is one feature on one platform. It’ll iterate, competitors will respond, and something else will be the discourse flashpoint in six months. The point is that understanding the underlying systems and understanding how they work isn’t optional anymore.

And the strategic question isn’t “how do I game the algorithm?” It’s broader than that. It falls into how do I position my music, my data, and my audience relationships to capture value across a system that is simultaneously the most powerful discovery mechanism ever built, and the most effective mechanism for extracting the economic value of fan relationships away from artists?

That requires operating on three levels simultaneously.

Understand the Discovery Architecture

Algorithmic playlists account for a significantly larger share of Spotify consumption than editorial playlists; by some analyses, roughly five times more. The industry massively over-indexes on editorial pitching relative to algorithmic discovery.

As AI mediates discovery, metadata is the new shopfront. Genre tags, mood descriptors, lyrical themes, geographic origin, among other things all feed the system.

As previously mentioned I have two full articles about this…

Build What You Actually Own

Owned audience and data is the capital that influences deals and career longevity. Discovery without conversion infrastructure is attention that evaporates.

Every listener moved from an algorithmic recommendation to your email list, Discord, or merch store is value no algorithm change or payout revision can touch.

No single platform should own your audience relationship. Multi-platform presence, single-destination ownership.

The Advocacy Agenda: Defence to Offence

Fan data portability. Platforms identify an artist’s most engaged listeners with extraordinary precision and share none of it. Campaign for actionable listener intelligence, not just aggregate dashboards.

Native artist monetisation tools. The largest uncaptured opportunity. Western platforms haven’t built tipping, tiered subscriptions, or social features because the current model already generates record profits. Changing that calculus requires coordinated pressure backed by data and international comparisons.

Is The Ground Is Shifting, But The Sky Isn’t Falling

The Prompted Playlist backlash was earned, but catharsis isn’t a strategy. The discourse cycle will move on; the structural questions won’t.

For artists, the immediate work is unsexy but essential; metadata, audience ownership, conversion infrastructure, and understanding that streaming is one part of a revenue architecture, not the centre of it. For industry bodies, the agenda needs to move from defence to offence; fan data portability, native monetisation tools, and policy informed by what’s already working elsewhere.

From a DSP perspective, Western platforms are leaving money on the table, and the data exists to prove it. Tencent didn’t build integrated monetisation out of goodwill; it built it because it generates more revenue per user. That’s the leverage point and it also keeps the content creators (artists) and their fans spending money within the ecosystem.

The algorithm didn’t eat the playlist, like how streaming didn’t end radio. It replaced one gatekeeping system with another. The question is whether artists and the industry will be positioned to capture value within it and have the first mover advantage with future evolutions.

Article Planning Notes, Resources & References

For a full list of the article planning notes, additional resources & references, please consider becoming a paid subscriber and join the subscriber chat!